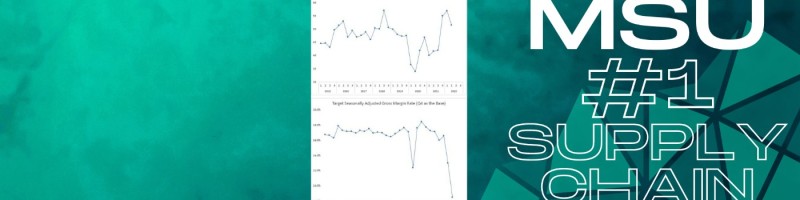

Wanted to pass along two plots that call into question the conventional wisdom that high inflation has wrecked consumers’ finances. Thoughts: •Top plot is from the New York Fed’s Survey of Household Debt & Credit, which uses a stratified random sample of credit reports to obtain data on the percentage of credit card balances that are 90+ days delinquent. As can be seen, this figure has actually been falling steadily from the start of the COVID-19 pandemic. Contrast this with the Great Recession and its immediate aftermath. •Bottom plot shows the delinquency rate on credit card loans as reported by all commercial banks to the Federal Reserve Board (https://lnkd.in/gn9-r-3X). In Q3 2022, this rate was 2.08%; for comparison, in Q3 2019, this rate was 2.62%. While we have indeed seen an increase from the all-time low of 1.55% in Q3 2021, what I believe is more significant is (i) the delinquency rate remains below pre-COVID levels and (ii) we aren’t seeing upward jumps like we saw in Q4 2008 or Q1 2009 (when the Great Recession was at its worst). •The same dynamic holds for mortgages: delinquency rates are actually trending down, with Q3 2022 being the lowest reading this side of the Great Recession (https://lnkd.in/gCNDFGU4). Implication: While credit card debt statistics receive the majority of media attention, there are many other data points suggest the U.S. consumer hasn’t been crushed by inflation. For anyone interested in those data points, check out https://lnkd.in/g8U94eb6 and the vast number of data series therein. #supplychain #supplychainmanagement #shipsandshipping #retail #freight #trucking

I don't think as many people are getting "crushed" because they are not losing jobs. They may be adjusting behaviors by spending less on discretionary items or by putting more $'s on debt, but they are not in a position to pay late or default - since they have a job (or can get a job or can get 2nd and 3rd jobs).

I would presume a contributing factor is that the extended student loan holiday is artificially supporting household cash flow levels.

Erik Sherman

1y

I'd disagree with your read on both graphs. Delinquency fell steadily after the Great Recession as well and for longer until the economy started to recover. Also, the pandemic saw massive amounts of aid and actual paydowns of credit balances. And notice that delinquency rates in the second graph are on the upswing as credit use also hits new highs. Delinquency rates on mortgages may be trending down because the number of new sales has imploded. That would leave more people with lower loans and greater degrees of built stability.

Let's see what it looks like after the Holidays.

I believe that the COVID lockdowns and layoffs forced consumers to look at their spending habits. Do you really need all that stuff?

Hello Jason, great information! What I’m curious about is how this data of credit card delinquency has been staved off by the increase in base wages. If base wages were to revert downward how would it affect delinquency and card use?

Savings rate & money velocity.

Can anyone think of some domestic policies that could have an immediate effect on the economy? First ten answers gets a steak at Erickson’s Smokehouse!

"Gradually, then suddenly."

1yNot sure if this is a good measure of financial well-being for the general public, the people who have credit cards to begin with are usually people already making more than the median income, unless we combine these data with the distribution of credit cards ownership by income bracket, it’s not that useful IMOH.